|

MGH Community News |

|

MGH Community News |

| September 2022 | Volume 26 • Issue 9 |

Highlights

Sections Social Service staff may direct resource questions to the Community Resource Center, Hannah Perry, 617-726-8182. Questions, comments about the newsletter? Contact Ellen Forman, 617-726-5807. |

Biden Clarifies Public Charge Rules

On September 8, 2022, the Biden Administration published a new federal regulation defining the meaning of “public charge.” This new rule formalizes guidance currently in effect, and marks a strong move away from the wealth test enacted under the Trump administration which led to widespread fear among immigrants and deterred millions from receiving the assistance for which they qualified. The new public charge rule is scheduled to take effect on December 23, 2022. Again, this new rule formalizes guidance the Biden Administration issued in March 2021 and hopefully will give immigrant households added reassurances that they can safely seek core safety-net benefits for which they and their dependents are eligible! Resources

|

- Adapted from [FoodSNAPcoalition] Biden Admin releases final "Public Charge" rules to protect immigrant households!, Pat Baker, MLRI, September 12, 2022.

SNAP for College Students – Expanded Access Below is a summary of the SNAP college student policy changes that DTA workers have been notified about, effective immediately!

DTA has elected a federal option to ignore ALL financial aid – including state, local and privately funded financial aid. This also means that students no longer need to document their non-federal financial aid or which portion is for educational vs living expenses. The "EDUC-1" form is eliminated. This is HUGE!

The DTA self-declaration policy takes a HUGE burden off students, college staff and DTA staff – it effectively ends the “paper chase.” A deep bow to DTA for issuing this guidance. - From [FoodSNAPcoalition] DTA expands SNAP access to college students, and impo updates from the Dept of Higher Ed! Pat Baker, MLRI, September 1, 2022.

SNAP Cost of Living Adjustment The nearly 550,000 Massachusetts households that receive SNAP benefits are about to see additional aid. Monthly benefits from the Supplemental Nutrition Assistance Program will rise by 12% starting in October, equating to a boost of about $25 to $30 per person per month, the Baker administration has announced. An individual who currently gets the maximum benefit of $250 per month will see their assistance rise to $281 on Oct. 1. The expanded relief comes as the federal government responds to mounting inflation, and as the Baker administration took into account rising energy costs that impact SNAP benefit level calculations. “SNAP is a critical tool in providing individuals and families with the financial power to buy food that meets their households’ cultural and nutritional needs,” Department of Transitional Assistance Acting Commissioner Mary Sheehan said in a statement Wednesday morning. “It also plays an important role as an economic stabilizer, providing an influx of federal dollars into the state’s economy, supporting our grocery stores, corner stores, local farms, and other food retailers. The increase in monthly SNAP benefit amounts will support the vital food security of many low-income households across the commonwealth and the communities in which they live, learn, and work.” Here’s a closer look at how maximum SNAP benefit levels will increase by household size: Household size: 2 Old amount: $459 New amount: $516 Household size: 3 Old amount: $658 New amount: $740 Additional pandemic-related SNAP benefits remain in effect, with a minimum payment of $95 each month. Bay Staters can see if they are eligible for SNAP benefits and apply online here. People can also call 877-382-2363 (press 7). “The Baker-Polito Administration continues to leverage every opportunity to tackle food insecurity and maximize federal nutrition programs,” Secretary of Health and Human Services Marylou Sudders said in a statement. “Increasing SNAP benefit amounts to reflect residents’ cost of living, in addition to continuing SNAP Emergency Allotments and implementing free school meals for all Massachusetts students this year, represents the Administration’s ongoing commitment to combating hunger across the commonwealth.” - See the full MassLive article.

Mayor Michelle Wu has appointed David Mayo as the new director for the Office of Returning Citizens, touting his combination of professional and lived experience as a perfect fit for the department, which focuses on helping incarcerated people re-enter society after leaving prison. The Office of Returning Citizens supports more than 3,000 people who return to homes in Boston each year from federal, state, and county prisons and jails. The appointment of Mayo, who succeeds longtime community outreach worker Kevin Sibley, is Wu’s latest step in bolstering the office, which was created in 2017 under former Mayor Martin J. Walsh. In April, Wu announced plans to boost the office’s previous $500,000 budget by $1.38 million. Her proposal was further expanded by Boston City Council during budget season, bringing the office’s total operating budget to $2.67 million for FY23, which began July 1. Drawing on his experiences working in South Carolina and here at the sheriff’s department, Mayo plans to employ a “wraparound case management” approach, which focuses on meeting four basic needs that often cause people leaving prison to struggle: housing, employment, education, and wellness. With an increased budget, Mayo said he intends to expand staffing and prioritize reaching incarcerated people and their families sooner, connecting them with resources before they are discharged when possible, and ensuring that basics are covered within days of their release. He also plans to move the office, which is located on Drydock Avenue in Seaport, into a neighborhood where residents are more directly affected by incarceration, and develop specialized programming for young adults and women. “We want to give them a backpack... with all the things they’ll need for their first two weeks: clothing, hygiene products, a map, MBTA cards,” he said. “That gives them that initial feeling of, ‘Hey, I can do a couple of weeks until I get my job.’” - See the full Boston Globe article.

Operator of Braintree, Plymouth Nursing Facilities Turned Away Patients with SUDs The operator of 21 skilled nursing facilities in the state, including in Braintree and Plymouth, could have to pay almost $100,000 in penalties after it turned away more than 500 patients who had prescriptions for opioid use disorder-related medications. Next Step Healthcare, which operates Braintree Manor Healthcare on Washington Street and Plymouth Harborside Healthcare, denied admission to 548 people who indicated they were prescribed addiction-related medications while seeking admission to Next Step’s programs, U.S. Attorney Rachael Rollins' office said. The people were not seeking addiction-related treatment. Those receiving treatment for a substance use disorder are generally considered disabled under the Americans with Disabilities Act, Rollins said, which prohibits private health care providers from discriminating on the basis of disability. Under a recently reached agreement with the U.S. attorney's office, Next Step must adopt a nondiscrimination policy specific to those with disabilities, provide training on disability discrimination and substance use to admissions personnel and pay a penalty of $92,383. If the agency complies with the terms of the agreement, the fine would be reduced to $10,000. - See the full Patriot Ledger article.

Court Ruling Supports Marijuana Expungement The Supreme Judicial Court of Massachusetts has ruled that a Boston judge “abused his discretion” when he denied a request by a former defendant to permanently erase legal records of two marijuana possession arrests in the early 2000s. The unanimous opinion, written by Associate Justice Serge Georges Jr., found that people previously arrested for cannabis crimes that have since been legalized are entitled to “a strong presumption in favor of expungement.” It orders a lower court to grant the request and effectively removes the power of state judges to deny similar petitions, unless they can cite a “significant countervailing concern.” The decision puts new muscle behind a 2018 reform law that nominally allowed former Massachusetts defendants to clear old criminal records resulting from one-off, low-level crimes committed before the age of 21, conduct that is no longer illegal (such as marijuana possession), cases of mistaken identity, or “demonstrable errors” by police, prosecutors, and judges. Lawmakers at the time hailed the measure as a significant step toward remedying past injustices and stark racial disparities in the state’s criminal justice system, saying the ability to destroy records of long-ago arrests and convictions that still appear on background checks would help former defendants secure jobs, apartments, college admission, and so on. Critics attribute the minimal impact of the law to several factors, including a lack of official outreach to former defendants and restrictive eligibility criteria. Another barrier has been a carve-out that allowed judges to reject even clearly eligible expungement applications without explanation by citing a fuzzy legal standard in the 2018 law: whether granting the petition would be “in the best interests of justice.” The seven-member court acknowledged that the law’s vague language lent itself to a “nearly endless number of plausible interpretations.” However, the justices concluded that the clear intent of lawmakers was to “make expungement more available where the Legislature has determined that the continued existence of those types of records would be unjust.” “In light of this legislative directive,” Georges wrote, “it would be a mistake to interpret ‘the best interests of justice’ provision as allowing judges wide latitude to deny otherwise-eligible... petitions for expungement.” The new ruling directs judges to make detailed written findings when they deny expungement requests, allowing the rejections to be appealed. And in expungement cases where the records cannot be completely destroyed because they concern other crimes that are ineligible for expungement, other defendants, or may be of use to an ongoing investigation, the SJC said judges should order them to be redacted. - See the full Boston Globe article.

Calculate How Much Your Mass. Tax Refund Check Will Be Eligible Massachusetts residents will see tax relief this fall, either through a check in the mail or direct deposit of about 13% of their 2021 personal income tax liability. No action is needed for Bay Staters to secure the tax credit, which is required under state law amid ballooning surplus revenues. Massachusetts residents who file their 2021 state tax returns on or before Oct. 17 are eligible for the refund, according to the Baker administration. The tax credit may be lower than the 13% of personal income tax liability — a figure that may change in late October once all 2021 tax returns are filed — if there are “refund intercepts,” including unpaid taxes and child support, among other variables. Residents can figure out their expected tax credit by visiting a state government webpage about Chapter 62F, the state law responsible for the taxpayer refunds. Or see the refund estimator on the webpage. The tool asks people to fill out tax information such as their earned income credit, child care and dependent care tax credit and senior circuit breaker credit, among other prompts. Residents can request a copy of their 2021 Massachusetts tax returns on this webpage to help fill out the refund estimator tool. A call center is available to residents weekdays from 9 a.m. to 4 p.m. by dialing 877-677-9727. Representatives won’t be able to share individuals’ refund amounts until the checks have been issued. - See the full MassLive article.

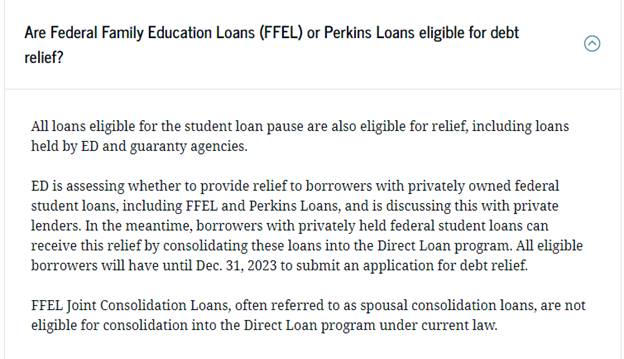

Student Loan Debt Cancellation Changes and Fact Sheet Student loan debt is one of the biggest contributors to the rise in the amount of debt held by older adults. The Biden-Harris administration and the U.S. Department of Education recently announced a number of initiatives to ease the debt load of federal student loan borrowers. This plan includes cancellation of up to $20,000 in student loan debt, an extension of the payment pause, and proposed changes to the income-driven repayment plan to make monthly payments more affordable. In addition, temporary changes to the Public Service Loan Forgiveness program, set to expire on October 31, 2022, make it easier for borrowers to qualify for the program. Read the National Center on Law & Elder Rights (NCLER) has issued a new Practice Tip that summarizes the recent announcements and upcoming important deadlines for cancellation of debt or other relief for borrowers with federal student loans. Advocates can use this information to help consumers navigate their student loan debt in the context of these new programs and relief. Excerpts Student Loan Payment Pause Extended Cancellation of Student Loan Debt Borrowers are eligible for debt cancellation if their individual income is less than $125,000 or $250,000 (for married couples or heads of households). Once the process opens, borrowers may receive relief automatically if the Department of Education already has their income data—such as if the borrower filled out the FAFSA or an income-driven repayment application in the past two years. However, most borrowers will have to apply. The Department of Education will launch an application process, which should be available by early October. Eligible borrowers are advised to apply early (at least before November 15th) to cancel debt before the student loan payment pause expires at the end of the year. Once a borrower completes the application, they can expect cancellation within 4-6 weeks. Nevertheless, if borrowers miss this window and their student loan payments resume in January 2023, they have until the end of the year, December 31, 2023, to apply for cancellation. To be notified when the process has officially opened, the Department of Education created a subscription page. NCLC’s Student Loan Borrower Assistance Project has more information on what borrowers need to know about cancellation. Public Service Loan Forgiveness Program (PSLF) The Department of Education made temporary changes to the program, which makes it easier for borrowers to receive credit for past periods of repayment that would otherwise not qualify for PSLF. Importantly, the waiver counts pre-consolidation time, which makes it easier for borrowers to obtain PSLF relief for Federal Family Education Loan and Perkins loans (both of which are excluded from PSLF relief under the normal regulations). However, these borrowers must consolidate their loans to have them included within a PSLF discharge. In addition, these temporary changes also make PSLF relief available to some Parent PLUS borrowers (who were generally ineligible for PSLF because Parent PLUS loans are not eligible for income-driven payment plans). Although Parent PLUS borrowers are excluded from the waiver, they can consolidate their loans with Direct Loans that have accrued eligible time, and the new consolidation loan will be credited with time that would have otherwise been available to the Direct Loan. Important PSLF Deadline These are time-limited changes that waive certain eligibility criteria in the PSLF program. These temporary changes expire on October 31, 2022. This is a hard deadline and applications after this deadline will not be eligible for the waiver. For more information on eligibility and requirements, go to PSLF.gov. In reversal, the Education Dept. Excludes Millions from Student Loan ReliefIn a remarkable reversal that will affect the fortunes of millions of student loan borrowers, the U.S. Department of Education has quietly changed its guidance around who qualifies for President Biden's sweeping student debt relief plan. At the center of the change are borrowers who took out federal student loans many years ago, both Perkins loans and Federal Family Education Loans. FFEL loans, issued and managed by private banks but guaranteed by the federal government, were once the mainstay of the federal student loan program until the FFEL program ended in 2010. According to federal data, more than 4 million borrowers still have commercially-held FFEL loans. Until Thursday of this week, the department's own website advised these borrowers that they could consolidate these loans into federal Direct Loans and thereby qualify for relief under Biden's debt cancellation program.

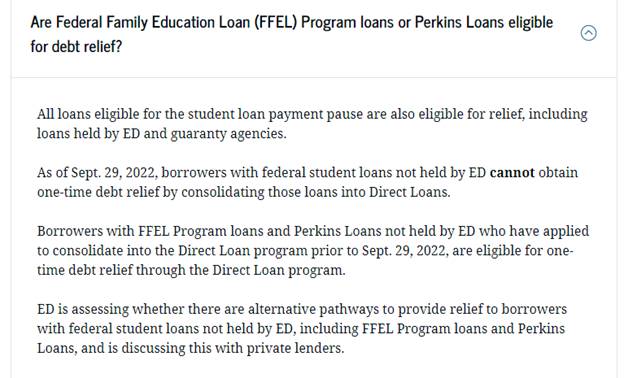

Original guidance: A screenshot of the U.S. Education Department's student loan relief guidance for holders of FFEL and Perkins Loans, taken at 10:16 a.m. on Thursday. On Thursday, though, the department quietly changed that language. The guidance now says, "As of Sept. 29, 2022, borrowers with federal student loans not held by ED cannot obtain one-time debt relief by consolidating those loans into Direct Loans."

New guidance: A screenshot of the U.S. Education Department's student loan relief guidance for holders of FFEL and Perkins Loans, taken at 11:39 a.m. on Thursday. It's unclear why the department reversed its decision on allowing FFEL borrowers with commercially-held loans to consolidate and then qualify for debt relief. In a statement to NPR, a department spokesperson says, "Our goal is to provide relief to as many eligible borrowers as quickly and easily as possible, and this will allow us to achieve that goal while we continue to explore additional legally-available options to provide relief to borrowers with privately owned FFEL loans and Perkins loans, including whether FFEL borrowers could receive one-time debt relief without needing to consolidate. Borrowers with privately held federal student loans who applied to consolidate their loans into Direct Loans before September 29, 2022 will obtain one-time debt relief. The FFEL program is now defunct and only a small percentage of borrowers have FFEL loans." The tell in that statement is "legally-available." Multiple legal experts tell NPR the reversal in policy was likely made out of concern that the private banks that manage old FFEL loans could potentially file lawsuits to stop the debt relief, arguing that Biden's plan would cause them financial harm. When FFEL borrowers consolidate their old loans into federal Direct Loans, these private banks essentially lose business. If these banks' financial health depends, at least in part, on the assumption that they would be holding and profiting from these debts over the long-term, then losing borrowers to Biden's debt relief plan could, possibly, constitute harm. Changing the policy now, and limiting the number of FFEL borrowers who can conceivably qualify for debt relief, may make these FFEL banks less likely to legally oppose debt relief. - From Cancellation of Debt & Other Changes to the Federal Student Loan System that Impact Older Borrowers, NCLER, September 20, 2022 and https://www.npr.org/2022/09/29/1125923528/biden-student-loans-debt-cancellation-ffel-perkins.

Team Impact Matches Pedi Patients with College Sports Teams Your child is going through something most 5-to-16-year-olds aren’t. But illness, disability, ongoing treatment, or extended hospital stays shouldn’t keep your child on the sidelines. With Team IMPACT, your child can experience positive social-emotional development through the support of a team. Let us match you with an encouraging, enthusiastic community to welcome and support your whole family on this journey. Eligibility Requirements:

More Information https://teamimpact.org/ and FAQs - Thanks to Kate Bernstein and Sarah Taddei for sharing this resource.

New College Student Health Insurance Options Flyer In Massachusetts, college students must have health insurance. Students will be enrolled in their school-based insurance, unless they have other coverage and waive the school-based insurance by their school's deadline. Students may be unaware that there are other health insurance options that may be more affordable than school-based insurance such as staying on a parent’s health insurance, MassHealth or purchasing a plan through the Connector. Mass Law Reform Institute (MLRI) has created a flyer Student Health Insurance, available in both English and Spanish, to explain options. - Adapted from [Health-announce] Student Health Insurance Flyer & Next HCWG Meeting, Kate Symmonds, MLRI, September 14, 2022.

Medicaid Waiver Makes Money Available for Housing, Nutrition The federal government has approved a five-year, $67 billion agreement with the state of Massachusetts that will govern how the state administers its Medicaid program. Gov. Charlie Baker said the so-called 1115 waiver is the primary way in which Massachusetts has historically been able to implement new, innovative programs within MassHealth, including paving the way for universal coverage. The latest agreement includes initiatives aimed at addressing social issues that affect health, like housing and nutrition, while also putting additional money into areas like primary care, behavioral health, and workforce training. The last state Medicaid waiver was approved in 2017. The new one goes into effect October 1 and will last through December 2027. Dan Tsai, deputy administrator for the Center for Medicaid and Medicaid Services, said the new initiatives in Massachusetts, as well as a waiver that was approved in Oregon, are about “thinking about the whole person when it comes to care.” Tsai touted as “groundbreaking” provisions implemented by both states that will let a certain population of Medicaid recipients maintain continuous coverage for more than a year without having to renew their coverage. Typically, people must renew their Medicaid insurance coverage annually and have their eligibility reconfirmed. (That has been suspended during the COVID public health emergency.) Tsai said many people lose coverage at the renewal date not because they are ineligible but because they don’t get the notification letter or do not take steps to renew their coverage. The Massachusetts waiver will let people who are homeless maintain continuous coverage for 24 months without having to renew their coverage. MassHealth members recently released from correctional facilities will get 12 months of continuous coverage without having to prove that they remain eligible. Another new approval included in the waiver will let the state use MassHealth money to incorporate social supports into the services it provides MassHealth recipients. Social supports could include food assistance and medically tailored meals or various types of housing support. The benefits will be tailored to certain vulnerable populations, including post-partum women 12 months after giving birth, children, and pregnant women. Money can also be used for transition support for individuals on MassHealth who are released from incarceration. Another major piece of the waiver is the authorization of $43 million over five years for loan repayment and residency training programs for behavioral health clinicians who will serve Medicaid patients. Baker said one of the biggest reasons people have trouble getting mental health appointments today is a lack of clinicians in the field – which comes back to a lack of funding for clinicians. There will be $115 million a year going into primary care, which Baker said will help the state expand the delivery system for primary care through a system that rewards team-based, high-value health care. There will be programs focused on improving the quality of care and ensuring equity within primary care delivery. A $2 billion, five-year initiative will hold private hospital systems accountable for reducing disparities in health care quality and access, including in maternal health. - See the full CommonWealth Magazine article.

Congressional Delegation Asks for Federal Help After $1 Million in SNAP Benefits Stolen from Low-Income Families With more than $1 million in Massachusetts SNAP benefits recently stolen, the state’s congressional delegation has urged U.S. Department of Agriculture Secretary Thomas Vilsack to help officials recoup the losses and strengthen security parameters to insulate low-income households from future theft. More than 2,000 Massachusetts households have been the victims of “skimming” within just two months this summer, according to a letter sent by the delegation — and helmed by U.S. Rep. Jim McGovern, chairman of the House Rules committee — to Vilsack earlier this month. While the USDA has told states they cannot rely on federal SNAP funds to restore stolen benefits, the letter urges Vilsack to “instruct states to restore benefits stolen through skimming and assure states that USDA will cover the cost.” Criminals engage in skimming as they duplicate credit and debit cards by placing card readers — which can be difficult for customers to detect — on ATMs or point-of-sale terminals. The practice also gives criminals access to people’s SNAP benefits. In a long-term solution, the delegation demands the USDA “move quickly to help states implement EBT technologies that are more secure than the current system and that are workable for households.” “The federal government mandated that states deliver benefits through EBT. The risk of skimming has been apparent for a number of years, but, to the best of our knowledge, USDA has not issued regulations or established standards to help states implement more secure systems,” the delegation said. - See the full MassLive article.

|