|

MGH Community News |

|

MGH Community News |

| May 2023 | Volume 27 • Issue 5 |

Highlights

Sections Social Service staff may direct resource questions to the Community Resource Center, Hannah Perry, 617-726-8182. Questions, comments about the newsletter? Contact Ellen Forman, 617-726-5807. |

Cambridge Will Start Giving Low-Income Families $500 Cash Monthly – Apply By July 31 The city of Cambridge will start giving low-income families $500 a month as part of a new guaranteed income program. City leaders and community members recently announced the new $22 million program, which is called "Rise Up Cambridge: Cash Payments for Families with Kids." The program, which builds on the city's previous pilot program, aims to combat poverty and income inequality by providing direct cash payments to families with children under the age of 21, and who earn at or below 250% of the federal poverty level. (For example, $75,000 for a family of four.) Eligibility is regardless of immigration status. Eligible families will get the $500 cash payments each month for 18 months. The city plans to explore ways to make the program more permanent, according to Cambridge Mayor Sumbul Siddiqui. The city will take applications for the program from June l until July 31, with payments expected to roll out by the end of June. It is the only guaranteed income program in the country that won't use a lottery to select participants, according to Siddiqui. "It is really for anyone who is eligible," she said. The city expects some 2,000 families will be eligible. Cambridge will fund its guaranteed income program using federal dollars from the American Rescue Plan with some money coming from the nonprofit Cambridge Community Foundation, Siddiqui said. Eligibility You are eligible if all of the following apply:

|

NOTE: Eligible Households include:

NOTE: If you or another adult in your household is attending full-time graduate school, pursuing a full-time professional degree (including but not limited to an MD, MBA, or JD), OR are a PhD candidate, you are not eligible for Rise Up Cambridge, even if you meet the other eligibility guidelines. There are no citizenship requirements.According to the United States Citizenship and Immigration Services, COVID-19 related benefits, including cash assistance, will not be used to determine whether or not an individual was or could become a public charge. FAQs What Counts as Income? Your public benefits do not count toward your household income. Some examples of public benefits include:

Please attend an in-person session to receive help calculating your income if:

My family is homeless and I do not have a permanent address. Can I apply? What documentation do I need? Do I have to report this money as income on my taxes? What happens if my income changes? What happens if my household composition changes? - See the full WBUR story and for more information see the Rise Up website

DHCD Now Known as the Executive Office of Housing and Livable Communities (EOHLC) As of Tuesday, May 30th, DHCD has finalized the transition to the Executive Office of Housing and Livable Communities (EOHLC). This is based on Governor Healey and Lt. Governor Driscoll filing Article 87 legislation earlier this year to establish a stand-alone secretariat focused on housing. The Executive Office of Housing and Livable Communities (EOHLC) was established to create more homes and lower housing costs in every region. EOHLC also distributes funding to municipalities, oversees the state-aided public housing portfolio, and operates the state's EA family shelter. Key Information:

- From Transition from DHCD to EOHLC, DHCD Partner Update, May 30, 2023 and https://www.mass.gov/orgs/executive-office-of-housing-and-livable-communities.

Metro Housing Introduces Housing Clinics Metro Housing's Housing Hub has introduced monthly Housing Clinics to the public. Future clinic dates, times, and registration information will be publicized on our Facebook page. These clinics will be staffed by the Housing Consumer Education Center and will assist in: *Housing Search (process, research, etc.) Housing Hub is Metro Housing's primary resource that is FREE and open to the public. Housing Hub staff help families address crises, educate and assist tenants and property owners. - From @HOME, Spring 2023, Metro Housing|Boston, May 16, 2023.

Replacing SNAP Benefits Lost to Skimming Since spring 2022, thousands of SNAP households in MA have had their SNAP stolen after thieves copied their EBT card and account information via “skimming” at a Point of Sale device in the checkout line. In December, Congress passed a law providing for federal funds for replacement for up to 2 months-worth of SNAP stolen on or after October 1, 2022. But as of May 12, no SNAP has been replaced yet for MA households who had their SNAP stolen after October 1st. In March, Governor Healey signed a supplemental budget providing state funds to replace benefits stolen before October 1, 2022. This month DTA took the first big step of making families whole who have been harmed by skimming. DTA issued replacement SNAP to households it knew had SNAP stolen before October 1, 2022. Those dollars should be available and on EBT accounts as of May 12! For more information see DTA’s press release. If any family whose SNAP was stolen before October 1 did NOT get a replacement payment for all of what was stolen before October 1, 2022, please let MLRI know! It may be that DTA didn’t know about their case. If any DTA client believes they may have fallen victim to a scam, they are encouraged to report it to DTA’s fraud hotline at 1-800-372-8399. Advocates may email Vicky Negus- vnegus@mlri.org. - From: Replacement SNAP for some skimming cases, Senate Ways and Means Budget Analysis, Victoria Negus, MLRI, May 12, 2023.

How to Check Your SNAP Balance- New Flyers Mass Law Reform Institute (MLRI) has created flyers to help members navigate the DTA Assistance Line and access their SNAP balance before they go shopping. Many older adults do not have a DTAConnect account and may be less comfortable with online navigation. There can be long wait times on the Senior Assistance Line, and the EBT customer service line can be equally daunting. Massachusetts Senior Action Council (MSAC) asked MLRI to create these step-by-step flyers to access current EBT balance information. Attached below is the original English version of the flyers, as well as a Spanish translation. Please let me know if you have any feedback from your clients or need additional resources. MLRI is currently in the process of translating these flyers into additional languages. DTA Assistance Line Translated Flyers - From DTA Assistance Line phone menu flyers prepared by MLRI and MSAC, Katie Kelly, MLRI, May 23, 2023.

The Homeowner Assistance Fund (HAF) Ending on June 30th The Massachusetts Homeowner Assistance Fund (HAF) is a state program that has been providing mortgage relief to homeowners who are behind on their mortgage payments due to the pandemic. This program will end on 6/30. Beginning on 7/1 the Residential Assistance for Families in Transition (RAFT) will once again be open to low-income homeowners that are at risk of foreclosure. At that time eligible homeowners will be able to apply for RAFT through the online portal. Currently, if households are facing an imminent foreclosure within the next 7 days, they should contact the Massachusetts Division of Banks (DOB). The DOB may be able to request a 60-day stay providing extra time for the homeowner to seek resources. And hopefully avoid foreclosure. More information about the HAF program and to apply, see: mass.gov/info-details/homeowner-assistance-fund-haf - Thanks to Hannah Perry for submitting this article.

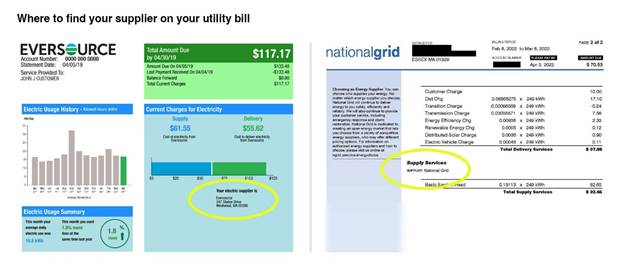

Tips to Avoid Losing Money or Getting Scammed by Competitive Energy Suppliers Massachusetts is one of about a dozen states where residents can choose to buy electricity from a supplier other than their default utility. When lawmakers set up this system in the late 1990s, the assumption was that a competitive marketplace would result in lower power prices for customers. But for the most part, the opposite has happened. Your utility typically charges you for two services: The power it buys on your behalf in the wholesale market and the cost of maintaining the wires that bring electricity to your home. Each of these things represents about half of your monthly bill. This system of “consolidated billing” was intended to make things simple for ratepayers, but it also makes it easy to miss that you have a competitive supplier, Devin MacGoy, a community organizer with the nonprofit GreenRoots said. “Many residents are surprised when I tell them that they are receiving their electricity from another company, because the bill comes from Eversource and the name of the [competitive] supplier is written on their bill in very small letters,” he said. It can be especially confusing for residents with limited English proficiency, he added. "What these companies do is, even if they offer a lower price to start with, they jack up their price later down the line," MacGoy said. "And so folks end up paying way more than they should be." About a decade ago, the Massachusetts Attorney General’s Office started getting a flood of complaints about competitive electric suppliers. When Nathan Forster, chief of the energy and telecommunications division, and his team started looking into the matter, they assumed the problem was limited to a handful of predatory companies. Turns out, it isn’t “a few bad apples.” Forster said the office has not found a single case of a company that has been able to charge customers less than a utility over a multi-year period. If people save money, it’s usually a couple dollars a month — and it's often because of temporary introductory rates. By contrast, the average consumer loses about $200 annually. While utilities are not allowed to make money on the power they supply you — they make money elsewhere — competitive supply companies need to profit on the sale of electricity. "And unfortunately, what happens is when you have [an industry] where the businesses can't make money honestly, they start making money dishonestly," he said. “I think the biggest thing that makes me frustrated about the competitive electric suppliers is that traditionally they have gone after the people who can least afford the predatory product that they're offering,” said Rev. Mariama White-Hammond, chief of environment, energy and open space in Boston. From what she’s seen as the city’s top energy official, suppliers seem to target people of color, lower-income residents, older adults, non-native English speakers and, increasingly, college students, many of whom are paying utility bills for the first time. State data bears some of this out. Using demographic information about which households qualify for subsidized electricity rates, the Attorney General’s Office has found that lower-income residents and communities of color are disproportionately harmed by this market. “I’ve had clients [who] had their utility shut off, or faced utility shutoffs, because of arrearages due in large part to paying more for a competitive supplier,” said Alexa Rosenbloom, an attorney in the Consumer Protection Clinic at Harvard Law School. She’s also had clients who couldn’t afford to cancel their plan because they would have to pay a few hundred dollars in termination fees. Instead, they ended up further in debt. One reason this market is so problematic is that these companies can charge ratepayers whatever they want, said Jenifer Bosco, a senior staff attorney with the National Consumer Law Center. “They can sign up customers for a variable rate contract and keep raising that variable rate higher and higher,” she said. State law also says that utilities must pay competitive suppliers what they’re owed every month, regardless of whether ratepayers can afford their bills. “The [supplier] is not responsible for any of that credit and collections work,” Bosco said. “They just literally can collect their money from the utility company at whatever rate they set.” This ultimately raises everyone’s bills. All ratepayers in the state help subsidize the discounted electricity rates low-income customers pay. And if those customers pay higher rates, the subsidy is also higher. According to the Department of Public Utilities, ratepayers throughout the state paid an extra $6 million in 2020 alone because of competitive supply rates for low-income customers. Tips to Avoid Getting Scammed by Competitive Suppliers Many of these companies use aggressive — and often deceptive — marketing tactics to get customers to enroll. But here are some tips to help you make informed decisions and avoid getting scammed: 1. Understand your supplier optionsMany Massachusetts residents actually have three electric supply options.

Note: Approximately 50 communities in Massachusetts are served by municipal light plants. These are like mini city-owned utilities, and they are different than municipal aggregators. If you live in a town that’s served by a municipal light plant, this is your only electric supplier option. 2. Learn to read your electric billIt’s not uncommon for people to have a competitive supplier and not know. When you sign up, nothing physically changes about your electric service and your monthly electric bill still comes from your utility. Your bill does say who your supplier is, but you have to know what you’re looking for to find it. Here’s where to look on an Eversource or National Grid bill:

If you look at your bill, you will see one of three things. Your supplier could be your utility, a competitive supplier, or a municipal aggregator. 3. Know who is on the phone or at your doorMany door-to-door salespeople or telemarketers are purposefully vague about who they are when they talk to you. While there have been documented cases of salespeople lying and telling customers that they work for a utility company, in many cases, they’ll say things like, “I’m working with your utility.” They are not. No one from Eversource, National Grid or Unitil will come to your door to talk to you about your electric rates. Utilities don’t do this. Salespeople may also hint (or say outright) that they work for your city or town. Consumer advocates say this often happens around the time a municipality launches an aggregation program. People may be aware that something is changing about their electricity, but they don’t understand the details. And competitive suppliers exploit this. 4. Don't show anyone your electric billIf salespeople come to your door and ask to see your bill, experts all agree: do not show it to them. Even if they say they want to see what rate you're paying and check if you’re being overcharged — don’t show it to them. If a person has your utility account number, it's possible for them to sign you up for a competitive supply plan without your consent. This is a practice known as “slamming.” It’s not clear exactly how common this is in Massachusetts, but experts say it does happen. 5. Consider putting yourself on the “do not switch list”If you’re totally freaked out about competitive suppliers and want some peace of mind, consider asking your utility to put you on the “do not switch list.” If you are on this list, the utility will not allow your account to be switched to a competitive supplier. To sign up, call your utility. 6. Check online to compare rates and contract termsIf you’re diligent about regularly comparing prices, it is possible to save some money with a competitive supplier. If you decide to enroll, experts say the first thing you should do is check the Energy Switch Massachusetts website. (Sometimes, the rates online are different than what door-to-door marketers offer.) This website, which is maintained by the Department of Public Utilities, can help you shop for a supplier. It allows you to sort by price or renewable energy content, and it tells you the contract terms for any given plan — how long is the contract for? Does it renew automatically? Is there a cancellation fee? The website also shows you the rates offered by your utility or municipal aggregator, which is always worth checking. Also, if you know how much electricity you use each month, you can enter that into the website and it will give you more accurate estimated price for your monthly bill. As you’re comparing plans, keep in mind that the rate you see may be an “introductory rate,” and that it could balloon after the contract renews. 7. Be aware of service feesSome competitive suppliers offer low electric prices, but charge a few hundred dollars a month in service or customer fees. A new report from the Massachusetts Attorney General’s Office found that residents paid about $5 million in customer fees between June 2020 and June 2021 — this is on top of their regular electric charges. The report also found that low-income residents were 28% more likely to be charged a customer fee than non-low-income customers. Make sure you read the fine print of any contract you sign. 8. Consider a municipal aggregation programThere are 176 communities in Massachusetts with a municipal aggregation program, and many offer lower rates than utilities. If you live in Boston, for example, the city offers power at about $0.11 per kilowatt hour, while Eversource’s rate through June 2023 is almost $0.26 per kilowatt hour. Municipal aggregation programs also use competitive supply companies, but because a city or town buys power in bulk and has the resources to hire lawyers and other experts to help negotiate contracts, they don’t end up with the same type of rates as individual customers who sign up. (For this same reason, consumer advocates say the competitive supply industry has worked well for commercial and industrial customers.) Many suppliers, including some municipal aggregation programs, also offer “green” or 100% renewable plans. If you’re concerned about the environment and willing to pay a little extra, experts say you are better off signing up for the municipal aggregation plan because there’s more transparency about where the power comes from and whether the supplier is using renewable energy credits to “offset” the non-renewable energy it’s buying. - See the full WBUR coverage:

Biden Administration Warns Consumers to Avoid Medical Credit Cards The Biden administration is cautioning Americans about the growing risks of medical credit cards and other loans for medical bills, warning in a new report that high interest rates can deepen patients' debts and threaten their financial security. In its new report, the Consumer Financial Protection Bureau estimated that people in the U.S. paid $1 billion in deferred interest on medical credit cards and other medical financing in just three years, from 2018 to 2020. The interest payments can inflate medical bills by almost 25%, the agency found by analyzing financial data that lenders submitted to regulators. "Lending outfits are designing costly loan products to peddle to patients looking to make ends meet on their medical bills," said Rohit Chopra, director of CFPB, the federal consumer watchdog. "These new forms of medical debt can create financial ruin for individuals who get sick." Nationwide, about 100 million people — including 41% of adults — have some kind of health care debt, KFF Health News found in an investigation conducted with NPR to explore the scale and impact of the nation's medical debt crisis. The vast scope of the problem is feeding a multibillion-dollar patient financing business, with private equity and big banks looking to cash in when patients and their families can't pay for care, KFF Health News and NPR found. In the patient financing industry, profit margins top 29%, according to research firm IBISWorld, or seven times what is considered a solid hospital profit margin. Millions of patients sign up for credit cards, such as CareCredit offered by Synchrony Bank. These cards are often marketed in the waiting rooms of physicians' and dentists' offices to help people with their bills. The cards typically offer a promotional period during which patients pay no interest, but if patients miss a payment or can't pay off the loan during the promotional period, they can face interest rates that reach as high as 27%, according to the CFPB. Patients are also increasingly being routed by hospitals and other providers into loans administered by financing companies such as AccessOne. These loans, which often replace no-interest installment plans that hospitals once commonly offered, can add hundreds or thousands of dollars in interest to the debts patients owe. A KFF Health News analysis of public records from UNC Health, North Carolina's public university medical system, found that after AccessOne began administering payment plans for the system's patients, the share paying interest on their bills jumped from 9% to 46%. "Patients appear not to fully understand the terms of the products and sometimes end up with credit they are unable to afford," the agency said. The risks are particularly high for lower-income borrowers and those with poor credit. The CFPB warned that the growth of patient financing products poses yet another risk to low-income patients, saying they should be offered financial assistance with large medical bills but instead are being routed into credit cards or loans that pile interest on top of medical bills they can't afford. "Consumer complaints to the CFPB suggest that, rather than benefiting consumers, as claimed by the companies offering these products, these products in fact may cause confusion and hardship," the report concluded. "Many people would be better off without these products." - See the full NPR story.

DHS Announces Upcoming Re-parole Process for Afghan Nationals The Department of Homeland Security (DHS) has announced it is establishing a process to re-parole eligible Afghan nationals so they can continue living and working legally in the United States. Beginning in June, Afghan nationals who arrived in the United States under humanitarian parole through Operation Allies Welcome (OAW) will be able to request a re-parole through online and paper filing. As with any parole request, these requests will be considered on a case-by-case basis for urgent humanitarian reasons and significant public benefit. Additional details regarding the process will be available soon. Afghan nationals are encouraged to pursue a permanent status in the United States for which they may be eligible, including through the Special Immigrant and Asylum processes, and should create or update online accounts on myUSCIS. Starting on May 17, DHS will begin to host Afghan Support Centers across the country; dates and locations for Afghan Support Centers will be announced in the coming weeks. See the full DHS Announcement:. - Thanks to Fiona Danaher for sharing this update.

New DDS Ombudsperson Meghan Allen is the new DDS Ombudsperson. An Ombudsperson can help resolve conflicts, offer guidance, and make sure individuals and families are receiving their eligible services. As Ombudsperson, Meghan plans to continue to expand upon her work with individuals, families, DDS and other stakeholders to remove barriers, increase opportunities and make Massachusetts a better place to live for individuals with intellectual and developmental disabilities. Contact Meghan Allen at: Meghan.L.Allen@mass.gov - From Department of Developmental Services Newsletter, DDS Massachusetts, May 31, 2023.

HousingMatch.org- A Non-Profit Roommate Listing Service Housing Match.org is a member-based, shared housing network. Membership is free and members can post if they are seeking a roommate(s), have a room in their home they are hoping to rent, or to list their property for rent. HousingMatch may be one short-term solution while waiting for subsidized housing – the site can connect folks allowing them to share rent costs until more permanent housing is available. For example, four individuals receiving SSI could potentially share a two-bedroom apartment. The only cost associated with HousingMatch is the cost of background check reports. Landlords and property owners posting rental properties that they do not live-in do not need to complete the background check reports. Housing Match does not screen the reports. They are used as a tool for potential roommates and renters. The HousingMatch website also provides additional resources including a sample housing rental agreement, roommate rental agreement, and a roommate interview questionnaire. More information can be found at: https://housingmatch.org/ - Thanks to Hannah Perry for submitting this article

Open Door Provides Medically Tailored Groceries in Gloucester and Ipswich Need help keeping your health on track? You may qualify for Medically Tailored Groceries, a program that couples one-on-one nutritional counseling with nutrition specific food boxes to help you stay healthy and active. Medically Tailored Grocery boxes contain fully prepped or partially prepped entrees, diary, produce and shelf-stable items along with recipes and suggestions for how to prepare food that will bring you life. Clients may need a physician’s referral. For an application - See their website Innovate | The Open Door (foodpantry.org)

MassHealth COVID Coverage After the End of the PHE MassHealth put in place many flexibilities during the federal Public Health Emergency (PHE) relating to COVID-19. This bulletin provides updated information on certain COVID-19-related services and flexibilities after the end of the PHE on May 11, 2023. Coverage for COVID-19 Vaccine Services for MassHealth Members Other than MassHealth Limited and HSN MassHealth will continue covering COVID-19 vaccine services for MassHealth members, at no cost to the member, after the expiration of the federal PHE. Coverage for COVID-19 Testing Services for MassHealth Members Other than MassHealth Limited and HSN MassHealth will continue covering COVID-19 testing services for MassHealth members, at no cost to the member, after the expiration of the federal PHE. PCR and antigen testing remains available for MassHealth members. In addition, over-the-counter (OTC) COVID-19 tests at MassHealth pharmacies will continue to be covered, but fewer per month MassHealth currently covers eight OTC COVID-19 tests per member per month without prior authorization. MassHealth expects to cover two OTC COVID-19 tests per member per month without prior authorization, beginning July 2023. If additional tests are medically necessary, prior authorization may be required. Coverage for COVID-19 Treatment Services for MassHealth Members Other than MassHealth Limited and HSN MassHealth will continue covering COVID-19 treatment for MassHealth members after the expiration of the federal PHE. There will be no copays for such treatment services through at least September 30, 2024. Delivery of Prescription Medications to MassHealth Members As described in Pharmacy Facts 167 and in 101 CMR 446.03(5): Prescribed Drugs, eligible pharmacy providers receive a payment adjustment to the professional dispensing fee when medications are delivered to a personal residence (including homeless shelters). This payment adjustment will continue after the end of the federal PHE. MassHealth will pay the delivery fee to a provider only once per member per day regardless of the number of prescriptions being delivered. The fee is payable only for deliveries to members living in personal residences and is not payable for claims for members living in any type of institution or residential facility, except for homeless shelters. Billing for COVID-19 Vaccines, Treatment, and Testing Services for MassHealth Limited and HSN During the federal PHE and continued through at least September 30, 2024, COVID-19 vaccine services are a covered service under MassHealth Limited. Effective May 12, 2023, COVID-19 testing will be covered for MassHealth Limited members to the extent performed in an emergency department. No other testing for COVID-19 may be billed for MassHealth Limited members after the end of the federal PHE. HSN providers rendering COVID-19 vaccines, treatment, and testing services to HSN patients (including for COVID-19 testing for MassHealth Limited members after the expiration of the federal PHE performed outside of an emergency department) should submit claims for such services to the HSN. This includes two over-the-counter tests for COVID-19 per patient per month. Transportation to COVID-19 Vaccine Appointments for Members in Family Assistance, CMSP, and MassHealth Limited, and for HSN patients As described in All Provider Bulletin 310, MassHealth provided transportation for members enrolled in Family Assistance, CMSP, MassHealth Limited, and HSN, for transportation through its Human Services Transportation (HST)’s regional transportation brokers to COVID-19 vaccination sites. Effective May 12, 2023, new requests for transportation for such individuals will no longer be approved. Transportation services to COVID-19 vaccine administration appointments and other covered medical services will continue to be available for MassHealth members in MassHealth Standard, CommonHealth, and CarePlus. Pharmacy Copay Suspension (also see next article) Effective May 1, 2023, MassHealth is suspending all pharmacy copays for eligibility groups consistent with 42 CFR 435 Subparts B, C, and D. This policy will remain in effect through March 31, 2024, and also applies to HSN patients. Children’s Medical Security Program (CMSP) members must still pay required copays. For the latest MA-specific COVID-19 information, visit the following link: www.mass.gov/coronavirus-disease-2019-covid-19. - See full MassHealth All Provider Bulletin 367.

MassHealth Pharmacy Copay Changes Effective May 1, 2023 Pharmacy Facts 199 announced that, effective May 1, 2023, through March 31, 2024, MassHealth members, including those in managed care plans, do not have to pay copays for prescription drugs. This also applies to Health Safety Net (HSN) patients during this period. Children’s Medical Security Plan (CMSP) members must still pay copays. There will continue to be no copays for members enrolled in One Care, Program for All-inclusive Care for the Elderly (PACE), and Senior Care Options (SCO) plans. Pharmacy Copay Poster Changes The pharmacy copay poster has been updated to reflect the new policy changes effective May 1, 2023, and can be found on the MassHealth Pharmacy Publications and Notices for Pharmacy Providers page, under the heading “Copay Poster.” - See the full MassHealth Pharmacy Facts.

Medicare to Cover Seat Elevation Technology for Power Wheelchairs The Centers for Medicare & Medicaid Services (CMS) announced this month that it will cover seat elevation technology in Medicare-covered power wheelchairs as durable medical equipment (DME). Effective immediately, both Original Medicare and Medicare Advantage will cover seat elevation for those who need it to perform activities of daily living in the home. This landmark decision meaningfully expands Medicare coverage and appropriately prioritizes enrollee independence and quality of life. The new coverage will apply when the individual has a specialty evaluation confirming they can use the equipment safely and when they need it for one of three conditions: (1) to perform weight-bearing transfers with or without caregiver assistance and/or the use of assistive equipment; (2) to perform non-weight bearing transfer to or from the power wheelchair in the home; or (3) to complete one or more mobility related activities of daily living such as toileting, feeding, dressing, grooming, and bathing in customary locations within the home. Other individuals, including those who do not use complex rehabilitative power-driven wheelchairs, may be able to gain coverage on a case-by-case basis. Despite the clear need many power wheelchair users have for technology that helps them safely transfer to and from the wheelchair and to better reach items and surfaces without joint or muscle strain, previously Medicare generally considered seat elevation in power wheelchairs to be a “mere accessory.” This categorization prevented coverage and downplayed the importance of features that help people maintain well-being, physical health, and community living. Future reforms could further improve access—CMS has indicated that it is also considering covering power wheelchair standing systems as DME. At Medicare Rights, we celebrate this important decision. We encourage CMS to cover standing systems as well, and to address other coverage gaps, including limitations on DME equipment for use outside of the home. Such technologies can help people live safely and independently in their communities. Read the coverage determination. - See the full Medicare Watch story.

Hospitals and Aid Groups Press State for Improved ‘Front Door’ To Emergency Shelter On any given night, the lobbies of hospitals in the Boston area have a clutch of people who are not there for health care. Rather, they are homeless, often newly arrived immigrants, looking for a safe, warm place to spend the night. But as the numbers escalate, hospitals and groups that work with migrants are pressing the state to expand access to emergency housing to help the city’s homeless families without drawing on critical hospital resources. “A hospital is not set up to be the front door to the state’s family shelter system,” a spokesperson from Boston Medical Center said in a statement. “BMC has urged the state to explore solutions that are open day and night, provide temporary shelter, and connect families to state and federal resources. It is critical that any solution address the magnitude of the crisis.” This month the Healey administration said it plans to spend $1.75 million on a new program called Immigrant Assistance Services. The money is enough for 800 individuals and families currently living in state-run homeless shelter placements and will include an intake and triage process to help immigrants with advice, legal services, and other supports. The state’s housing agency is also ramping up supports. A spokesperson for the Department of Housing and Community Development said the agency is hiring 60 additional staff. The agency is also trying to improve a call center, which receives the majority of contacts and applications for shelter. Larry Seamans, chief executive of Boston-based FamilyAid, said his human services agency has helped 175 families, more than 550 people, find emergency housing since last July, all of whom came directly from BMC. FamilyAid has been helping BMC since the COVID pandemic, when people who had lost their homes because of the economic upheaval would go to the hospital for shelter. With funding from the city, FamilyAid began providing temporary housing for families who showed up at BMC and Boston Children’s Hospital in the middle of the night. At the time, 65 percent of the families seeking shelter through the hospitals were Massachusetts residents and US citizens. Other hospitals are also helping growing numbers of homeless families. Mass General Brigham, the state’s largest health system, said in a statement that there has been an increase in families from Haiti and Central and South America seeking shelter and medical care in its emergency and obstetrics departments. Part of the reason families may be redirected to BMC is because the typical offices where they apply for emergency shelter are only open during business hours. Processing centers run by the Department of Housing and Community Development are open weekdays only, and some locations are open even fewer days, from 8 a.m. to 5 p.m. The agency’s call center also operates on business hours. Seamans of FamilyAid said emergency housing resources need to be open and accessible when families need them. - See the full Boston Globe article.

State Moves to Limit Local Government Limits on Family Shelter Facing pushback from some communities, the Healey administration is adopting a new housing code that explicitly exempts emergency shelters from certain state sanitary code requirements that could be used by towns to prevent hotels, motels and other properties from being used to accommodate the swelling tide of homeless and migrant families. While many communities have pledged to welcome those families, a number have bristled at hosting a surge of new residents, even temporarily. Some point to local ordinances that restrict the length of hotel stays or cite the lack of funds for schools that would be stretched with an influx of new families. The resistance from the towns adds another roadblock to the state’s effort to house homeless families amid a housing shortage that makes it difficult and very expensive to provide shelter. “We need every community to be part of the solution by welcoming families into shelter and building more affordable housing so we can address the root cause: a sustained, substantial housing shortage,” Samantha Kaufman, a spokesperson for the Department of Housing and Community Development, said in a statement. The state’s 1983 “right-to-shelter” law obligates officials to immediately house eligible families, pushing officials to find shelter options on short notice. At the same time, the number of migrants arriving from troubled places such as Haiti is escalating. The state has converted around 20 hotels into temporary emergency housing, and is actively identifying hotels, vacant college dormitories, or other potential solutions. But the efforts to expand that portfolio have been inhibited by local ordinances, which officials say make it difficult to move quickly. The Healey administration’s new housing rule is intended to address provisions such as those, exempting temporary shelter from a section of state law that dictates housing and occupancy standards under the Department of Health. The change, which was made in October, goes into effect May 12. State officials said the change should ameliorate some of the trouble it has had with certain towns. The new rule clears up language that state officials say some municipalities have misinterpreted when enforcing state law. The change means that municipalities will no longer be able to try to shut down shelters for failing to meet statewide sanitary requirements that apply to dwelling units but not homeless shelters, state officials said. The common refrain from communities is that shelter occupants would clog traffic, overwhelm schools, or threaten public safety. To advocates, the real reason behind local resistance arises from knee-jerk concern that shelters will negatively affect property values. To combat some of that criticism, the state has attempted to sweeten the deal for cities and towns. In March, Governor Maura Healey signed a supplemental spending bill that includes $85 million for the emergency assistance program, including nearly $22 million for schools that experience an influx of children from shelters. “We need to counteract some of the local opposition and misunderstanding around what the community impact would be by welcoming families,” said Kelly Turley, who has long advocated for such funding as director of the Massachusetts Coalition for the Homeless. And that work has made an impact, Turley said. Correction: An earlier version of the story incorrectly characterized the impact of the state’s new housing code. The new housing code clarifies that homeless shelters are exempt from statewide sanitary requirements that apply to dwelling units. - See the full Boston Globe article.

Vermont Becomes First State to Waive Residency Requirement for Medical Aid in Dying Vermont is the first state in the country to officially allow non-residents to request medications to hasten their death. Republican Gov. Phil Scott signed a bill into law Tuesday that removes the residency requirement from Vermont’s medical aid in dying law, which originally passed in 2013. Before today, only legal residents of the state could request prescriptions for the lethal medications from Vermont doctors. According to state data, 173 Vermonters used medical aid in dying between May 2013 and December 2022. The change comes after a Connecticut woman sued Vermont in order to access medical aid in dying. Lynda Bluestein reached a settlement with the state in March, under which the state waived the residency requirement for her. The case also prompted lawmakers to look into making the change permanent. Vermont is one of just 10 states and the District of Columbia where medical aid in dying is legal. Under state law, a person wishing to access life-ending medication must follow strict procedures, including getting two doctors to confirm a terminal diagnosis of six months or less to live. Oregon is also no longer enforcing its residency requirement, following a lawsuit that was settled last May. A bill to formally remove the requirement has cleared the Oregon House and is awaiting action in the Senate. - See the full WBUR story.

US Mexico Border Restrictions End, but New Restrictive Asylum Rules Begin President Joe Biden’s administration this month began denying asylum to migrants who show up at the U.S.-Mexico border without first applying online or seeking protection in a country they passed through, according to a new rule. The rule came just a day before the U.S. ended use of Title 42, which had allowed it to limit migration in the name of preventing the spread of COVID-19. The change has led to concerns about whether the U.S. has the necessary tools to control migration. The rule is part of new measures meant to crack down on illegal border crossings while creating new legal pathways, including a plan to open 100 regional migration hubs across the Western Hemisphere, administration officials said. The Asylum Ban applies only to those individuals who enter by land or sea at the U.S. Mexico border. The COVID-19 pandemic-related restrictions have allowed border officials to quickly return people — and they did so 2.8 million times since March 2020. But after the restrictions expired, migrants caught crossing illegally will not be allowed to return for five years. They can face criminal prosecution if they do. While stopping short of a total ban, the new policy imposes severe limitations on asylum for those crossing illegally who didn’t first seek a legal pathway. It includes room for exceptions and does not apply to children traveling alone. It was first announced in February and took effect on May 11, 2023. It’s almost certain to face legal challenges. A federal appeals court prevented similar but stricter measures pursued by then-President Donald Trump in 2019 from taking effect. Human rights groups said they plan to sue quickly. “This rule will subject people to grave harm,” said American Civil Liberties Union lawyer Katrina Eiland. She said it would result in migrants stranded in northern Mexico. She said the rule was predicated on the idea migrants can get protection in another country or get an appointment online to seek asylum in the U.S. She said there are serious problems with both those options. The Biden administration emphasized the complex dynamics at play when it comes to immigration that at one time consisted largely of adults from Mexico seeking to come to the U.S. They could easily be returned home. Now migrants come from across the Western Hemisphere and beyond. The rule was immediately met with criticism. “With its new rule formalizing sweeping restrictions on asylum access, the Biden administration is putting border politics ahead of the safety of refugees," said Jeremy Konyndyk, the president of Refugees International. U.S. officials also said they planned to open regional hubs around the hemisphere, where migrants could apply to go to the U.S., Canada or Spain. Two hubs were previously announced in Guatemala and Colombia. It’s unclear where the other locations would be. The administration officials spoke on the condition of anonymity to discuss ongoing border plans that were not yet public. The Democratic administration will return migrants from Haiti, Venezuela, Cuba and Nicaragua to Mexico if they do not apply online, have a sponsor and pass a background check. It will admit 30,000 per month from those nations to the U.S. Mexico will continue to take back the same number who cross illegally. Immigration officials also plan to deploy as many as 1,000 asylum officers to conduct expedited screenings for asylum seekers to more quickly determine whether someone meets the standard to stay in the U.S. Mayorkas said migrants taken into U.S. custody will be given an initial option to voluntarily turn back because of the increased consequences of removal after Title 42 expires. Most of the people going to the U.S.-Mexico border illegally are fleeing persecution or poverty in their home countries. They ask for asylum and have generally been allowed into the U.S. to wait out their cases. That process can take years under a badly strained immigration court system, and it has prompted increasing numbers to go to the border hoping to get into the U.S. Authorities have spent months setting up interview rooms and phone lines at facilities along the border to facilitate screenings, part of a broad effort to expand the use of expedited removal proceedings aimed at migrants who cross illegally into the U.S. - Sources and for more information:

Look Behind the Pharmacy Benefit Manager Curtain Secret transactions, billions of dollars involved, hidden tactics. Sounds like the next big movie mega hit. But it’s not. It’s actually the world of pharmacy benefit managers, or PBMs. You might not have heard of them, but they know a lot about your health care coverage. In fact, they orchestrate which drugs you have access to and how much you pay. Who are they and how did they get this power? That’s exactly what federal and state lawmakers are now asking and PBMs don’t like it. PBMs were supposed to help health insurers file claims, maintain pharmacy networks, and negotiate discounts on medications. The idea was that those discounts would help lower costs for patients. But that never happened. In fact, costs increased. Over the years, PBMs have amassed an enormous amount of power and they’ve consolidated that power with the acquisition of pharmacies. Working in tandem with insurers, they’ve been optimizing their profits making literally billions of dollars on the backs of patients. The three largest PBMs—CVS Caremark, Optum Rx and Express Scripts—now control about 80 percent of the drug market. That equates to 4 out of every 5 prescriptions being controlled by those three PBMs. Additionally, they and insurers own retail pharmacies, mail order pharmacies, and specialty pharmacies and steer patients to them. Because PBMs push patients to their own pharmacies, they have jeopardized the viability of independent pharmacists by reducing business and cutting reimbursement to levels that are less than the cost to obtain the medication. Many of these pharmacies, which for many underserved populations are the only touchpoint of health care, have closed. It has caused pharmacy deserts in underserved and rural areas. Originally promising to lower health care and drug costs, PBMs are finding themselves under scrutiny for things such as increasing costs, clawing back discounts, blocking copay assistance from counting towards a patient’s out-of-pocket costs, and charging states’ Medicaid programs significantly more than a medication costs —something the taxpayer is on the hook for. It’s patients who suffer thanks to the games PBMs play. Research has shown PBMs are raising drug costs to the point where sometimes it’s cheaper to pay cash than to go through insurers. Research found in some cases that going through the insurer (and thus the PBM) increased drug costs by 21 percent. And for 1 in 4 prescriptions the copays were higher than the cost of the certain drugs. How did things get so out of control? It’s simple. PBMs lack transparency and accountability and are unregulated. In fact, they are the only part of the health care distribution system that isn’t monitored. This month the US Senate Committee on Health, Education, Labor & Pensions is considering legislation that would create new reporting requirements for health plans and PBMs and ban policies that put middlemen profits over patients. The Senate Finance Committee and the Federal Trade Commission are also investigating the negative impact of these Goliath entities and the role PBMs play in raising drug costs. And in states across the country, including here in Massachusetts, there are bills pending that would look behind the PBM curtain. Unfortunately, the real victims in the PBM schemes, are patients who have seen their out-of-pocket costs skyrocket and access to medications restricted. All this should serve as a clarion call for our lawmakers to act immediately to increase transparency and accountability around PBMs, regulate them, and protect their constituents. - See the full Commonwealth Magazine opinion piece. |